by Colin Moor, CAIB | Sep 29, 2014 | Research Centre

LET’S SAY YOU OWN A RESTAURANT AND SUFFER A FIRE LOSS. YOU ARE FORCED TO CLOSE FOR TWO MONTHS TO MAKE REPAIRS AND THEN YOU FIND IT TAKES ANOTHER TWO MONTHS BEFORE YOUR BUSINESS RETURNS TO ITS NORMAL LEVEL. HOW CAN YOU PROTECT YOUR PROPERTY AND YOUR BUSINESS?

In this situation, your property policy pays to repair the building and replace your contents.

Your business losses (loss of income) are covered depending on the type of Business Interruption Insurance you’ve chosen.

If you have Gross Profits Insurance, your loss of income is paid while closed for repairs and while you rebuild your business to its original level, up to the limit of coverage.

On the other hand, Gross Earnings Insurance only covers the income lost during the time required to repair the premises.

If you own rental income property, you also have two choices for Business Interruption Insurance.

Gross Rentals Insurance acts on the same basis as Gross Profit Insurance. If your apartment building suffered a fire, your Gross Rentals Insurance will pay for the loss of income during the repair period and for lost income during the time it take to rent all of the damaged apartments up to the limit of coverage.

Whether your business is retail, restaurant, manufacturing or rental properties, we can offer the appropriate Business Interruption Insurance to protect you from loss of income. Call us to get started.

by Eddie Rodriguez, CAIB | Aug 30, 2014 | Research Centre

WHEN IT COMES TO INSURANCE, THERE ARE MANY DETAILS AND REQUIREMENTS THAT ARE NOT OFTEN THOUGHT OF UNTIL YOU ARE FACED WITH A CRISIS SITUATION, AT WHICH POINT IT IS OFTEN TOO LATE.

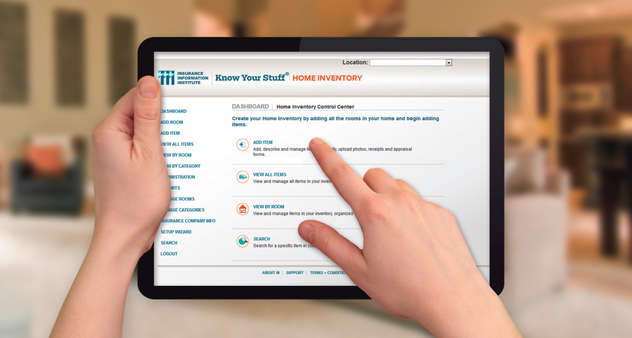

One such detail is that you are required to provide a schedule of contents lost or damaged as part of a claim.

- This schedule requires information such as:

- A description of the item(s);

- Date purchased and where the item(s) were purchased;

- Purchase price;

- Current replacement cost;

On the surface, this seems like a pretty straightforward and simple task, but disasters always have a tendency to strike when least expected. Imagine coming back from vacation to your home or business and finding nothing but a pile of burnt rubble. Once the initial steps in the claim process have been taken care of, you will now be required to provide a list of items lost in the claim.

Where do you begin and how are you going to ensure that you are fully indemnified for your loss? Will you remember every single item that was inside your home or business?

Not likely.

A great preventative measure to help ensure an accurate and prompt claim settlement is to complete a home or business inventory ….. now. Before it’s too late!

Although initially an inventory does require some work, it is an invaluable tool in the event of a crisis.

In addition to ensuring that all contents can be listed and included in a claim, an inventory will ensure that you are carrying an appropriate amount of coverage on your personal property or business contents.

SOME QUICK TIPS WITH RESPECT TO INVENTORIES:

- To save time, use digital photos or video if available. Something is better than nothing.

- Make sure you update the inventory from time to time, perhaps at renewal time. A 5 year old inventory is not likely to be accurate.

- Keep a duplicate copy offsite. As your broker, we’d be happy to help you by keeping a copy of your inventory in your file.

Don’t risk financial loss or down time. Complete an inventory for peace of mind.

And if you’re not sure where to begin, contact us, and we will e-mail you a copy of an easy-to-follow inventory checklist.

by Eddie Rodriguez, CAIB | Jul 26, 2014 | Research Centre

DON’T LET A TORNADO BLOW YOUR ASSETS AWAY

ON AUGUST 21, 2011, THE FIRST F3 TORNADO IN OVER 15 YEARS HIT THE LAKESIDE TOWN OF GODERICH, ONTARIO, CAUSING OVER $75 MILLION DOLLARS IN DAMAGE. LIKEWISE, ON JUNE 6, 2010, AN F2 TORNADO WENT FROM HARROW THROUGH KINGSVILLE AND LEAMINGTON, ONTARIO, BEFORE DISSIPATING NEAR POINT PELEE NATIONAL PARK, CAUSING $120 MILLION DOLLARS IN DAMAGE.

These tornadoes are a vivid reminder of the threat windstorms pose to life and property, as well as emphasize the importance of having the right insurance coverage.

No matter where you live, you need to have the right amount and type of insurance in order to recover financially after a natural disaster.

Across Canada, Ontario, Alberta, Manitoba and Saskatchewan average the most tornadoes per season, at approximately 15, followed by Quebec with less than 10. New Brunswick and the interior of British Columbia are also recognized tornado zones. All other provinces and territories have significantly less threat from tornadoes. The peak season in Canada is in the summer months when clashing air masses move north, although tornadoes in Canada have occurred in spring, fall and in the rarest of cases, winter. This differs from the United States’ southern-central plains, when spring is the most prominent season for tornadoes.

For a variety of reasons, such as Canada’s lower population density and generally stronger housing construction, due to the colder climate, Canadian tornadoes have historically caused fewer fatalities than tornadoes in the United States.

The standard homeowners and business insurance policy covers wind damage including that caused by tornadoes to the structure of the building and contents including broken windows and removal of debris.

However, you should make sure your coverage limits reflect the cost of rebuilding the structure, removing the debris and fully replacing personal belongings.

It’s important to make sure you have purchased ‘replacement cost coverage’ on your business policy and your homeowners’ insurance policy. If you have a business policy, it is also important that you carry ‘blanket bylaws coverage’ on your policy.

A homeowners’ policy also provides ‘Additional Living Expense (ALE) coverage’ to pay the costs of living away from home if you cannot inhabit your house due to damage from an insured disaster.

The policy ALE provision covers hotel bills, restaurant bills, and other living expenses incurred while away from your home, while it is being repaired or rebuilt.

‘Guaranteed Replacement Cost (GRC)’ or ‘Additional Rebuilding Cost (ARC)’ is another homeowner’s insurance coverage that can provide extra coverage, over and above the limit you have on your home insurance policy.

For example, let’s say you have your home insured for $400,000 – a tornado destroys 200 homes in your area, and building costs and inflation cause the replacement of your home to be $450,000. The GRC and ARC coverage’s would pay this additional amount subject to the terms and conditions of your policy. Make sure you review these coverages with your broker.

If you own a business that has been damaged, ‘business interruption coverage insurance’ is important to make sure you have revenue to continue to make your payments when a tornado has impaired your business. There are many different forms of business interruption, and as a business owner, you should review this on a regular basis with your insurance broker.

Damage to cars, trailers, motor homes and ATV’s are covered under the ‘comprehensive optional coverage’ portion of the policy. Marine insurance policies will usually cover damage to boats from wind.

Please make sure you review your insurance policies with your insurance broker on a regular basis to make sure your assets don’t get blown away, should a Tornado destroy or damage your home and business. With changing weather patterns, your home could be the next target.

For more information on your coverage options, call your insurance broker.

by Eddie Rodriguez, CAIB | Dec 13, 2012 | Research Centre

Let’s be honest: Even if you have a good understanding of what insurance does for you or for your business, deep inside, we all believe that peace of mind should be free, and that we shouldn’t have to pay a “premium” to enjoy it.

In reality, though, we all know that our modern society would not be able to function without the safety net provided by insurance.

As you attempt to achieve your company’s goals you will naturally take a number of risks that may bring about accidental losses (to your property, your income, through liability to others, etc.).

While some losses you may be able to absorb (pay for) yourself, in many cases you will want to ‘transfer the risk’ and costs associated with those loses to someone else: an insurance company.

Click here to see some some scenarios where you would be happy that the risk was transferred to an insurance company, and that the loss did not directly impact your company’s ability to survive and grow.

By the way, risk management is not merely about insurance.

Insurance is simply one of many ‘risk management techniques’ you’ll need to implement in order to achieve your growth and profitability goals.

Still, a day doesn’t go by without someone telling me that they really don’t enjoy – OK, they hate – paying for something they can’t see or touch, and hope they never have to use.

So, what could possibly be worse than paying for insurance?

Paying for it month after month, year after year … believing that “you’re covered”, only to find out – when the unexpected happens – that you are NOT.

Ouch!

How do you prevent that from happening to you?

Here’s the most important message I want to share with you in this article: Traditional ‘business insurance’ and traditional “Commercial General Liability” (CGL) policies are not sufficient to protect technology businesses against what I call “The Monsters” (risks).

In fact, as an IT consultant, software developer, game developer, web designer, owner/executive in charge of a data centre or other type of tech business you face risks that are usually excluded from coverage in regular business insurance policies.

Regardless of how mysterious, complex, or boring you find insurance, you must make sure that your policy provides coverage for the types of risks your technology business is exposed to.

Some of the coverages that you may need include:

- Technology-Specific Errors & Omissions

- Copyright or Trademark Infringement Liability Protection

- Property – Including, as needed, EDP Property and R & D Property

- Network and Information Security Liability

- Reputation Injury and Communication Liability

- Business Interruption

- Commercial General Liability

- Equipment breakdown coverage

- Media Liability Protection

Also, ask your broker to show you that the policy definitions of “business activities” actually match what your business does, and if not, ask if the policy allows for inclusion of your own definitions.

It’s true that properly insuring an IT business can be tricky. Our industry has product managers at insurance companies struggling to figure out ways of covering you from “social-media risks” and other Monsters that didn’t exist a few years ago.

The good news is leading insurance companies are finally paying attention. They’ve developed quality insurance products designed specifically to protect tech companies.

By the way, I know that some smaller tech firms try to get by without proper “risk transfer” (insurance) plans.

If you know anyone operating without an insurance safety net, please remind them that one of the truly sad realities of today’s business world is that you can be sued … even when you didn’t do anything wrong … and even after your software or service performed as expected.

Sure, you might win the lawsuit … after trading a big chunk of your hard-earned money for legal defense fees.

In fact, legal costs generally represent a large portion of the overall Professional Liability claims cost. That’s due to the need for expert (read: more expensive) witnesses and lawyers.

Bottom line – given the complexities of a technical business it makes sense to seek out well-designed, technology-specific insurance coverage from insurance companies – and brokers – who specialize in technology. That is the first step in eliminating any looming doubts about whether or not you are covered.

by Eddie Rodriguez, CAIB | Jul 20, 2011 | Research Centre

You’ll be happy to know that we work with several insurance companies who offer specialized insurance policies and coverages for the IT industry.

Because not all insurance companies (or their IT products) are the same, we’ve done the homework for you and have sourced out leading insurers that cater to various sub-segments of the the IT industry … from one-person firms to large multi-national companies.

Here’s are the types of IT businesses we work with – Is yours listed?

- I.T. Consultants

- Software and game developers

- Computer Training

- Data processors

- Data Storage/Retrieval Services

- Website Developers

- Web hosting and design facilities

- Access providers and co-location facilities

- Systems integrators, value-added resellers, and consultants

- Hardware, equipment & component manufacturer / assemblers

- Hardware Sales & Support

- Medical technology companies

- Internet, networking and other communications services.

and also:

- Telephone operations

- Telegraph operations

- Personal communications services

- Cable system operations

- Telecommunications component and equipment manufacturers

- Information service providers

- Interactive media services

- Telecommunications infrastructure development projects.

If you’re not sure if your type of IT business fits into one of the above categories, go ahead and contact us, using this brief online form.

The key thing to remember is that we can custom-tailor an Insurance Protection Plan that fits your needs.