by Eddie Rodriguez, CAIB | Aug 30, 2014 | Research Centre

WHEN IT COMES TO INSURANCE, THERE ARE MANY DETAILS AND REQUIREMENTS THAT ARE NOT OFTEN THOUGHT OF UNTIL YOU ARE FACED WITH A CRISIS SITUATION, AT WHICH POINT IT IS OFTEN TOO LATE.

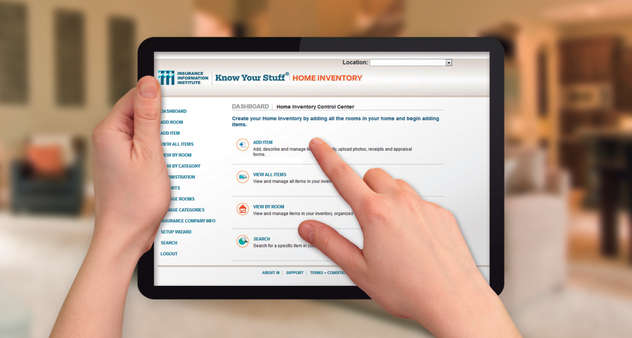

One such detail is that you are required to provide a schedule of contents lost or damaged as part of a claim.

- This schedule requires information such as:

- A description of the item(s);

- Date purchased and where the item(s) were purchased;

- Purchase price;

- Current replacement cost;

On the surface, this seems like a pretty straightforward and simple task, but disasters always have a tendency to strike when least expected. Imagine coming back from vacation to your home or business and finding nothing but a pile of burnt rubble. Once the initial steps in the claim process have been taken care of, you will now be required to provide a list of items lost in the claim.

Where do you begin and how are you going to ensure that you are fully indemnified for your loss? Will you remember every single item that was inside your home or business?

Not likely.

A great preventative measure to help ensure an accurate and prompt claim settlement is to complete a home or business inventory ….. now. Before it’s too late!

Although initially an inventory does require some work, it is an invaluable tool in the event of a crisis.

In addition to ensuring that all contents can be listed and included in a claim, an inventory will ensure that you are carrying an appropriate amount of coverage on your personal property or business contents.

SOME QUICK TIPS WITH RESPECT TO INVENTORIES:

- To save time, use digital photos or video if available. Something is better than nothing.

- Make sure you update the inventory from time to time, perhaps at renewal time. A 5 year old inventory is not likely to be accurate.

- Keep a duplicate copy offsite. As your broker, we’d be happy to help you by keeping a copy of your inventory in your file.

Don’t risk financial loss or down time. Complete an inventory for peace of mind.

And if you’re not sure where to begin, contact us, and we will e-mail you a copy of an easy-to-follow inventory checklist.

by Eddie Rodriguez, CAIB | Aug 30, 2014 | Research Centre

Did you know that a simple review of your policy can save you money?

Time and time again you will have received your renewal and seen the rates increase, but your pay may not have. This can be tough and we understand, as we are insurance consumers as well as advisers for you.

What you should ask yourself is, “Am I getting all I can from my insurance company?”

You may be thinking that call to your broker may cost you more rather than save you money. Some areas in which you may be able to take advantage of discounts could include the following:

- Upgrades to your roof, plumbing, wiring and heating

- Being mortgage free

- Installing an alarm system

- Being a non-smoker

- Installation of a sump pump

- Installation of a back-water valve (See video)

While many homeowners, condominium owners and secondary homeowner policies provide you with guaranteed replacement cost, there is the possibility that the guaranteed replacement cost endorsement could be null and void if you have not recently completed an updated rebuilding evaluation.

Over the years the calculation tools used to determine the rebuilding cost of your dwelling have been refined. This enables insurance companies to properly insure your residence in case of a loss and to make sure you get back all that you are entitled to.

Be sure to call your broker for more details on how the guaranteed replacement cost endorsement applies.

There are always pros and cons in making the decision to take a look at how much you should be insured for. Ask yourself, “How important is it to me to have peace of mind knowing I am “insured to value” in the event of a loss?”

There are even some companies that provide discounts when completing a new evaluation of your home.

This is also a good time to see what other coverages are offered by your insurance company. So take a deep breath, pick up the phone and you never know how much you can save unless you call us.

by Eddie Rodriguez, CAIB | Jul 26, 2014 | Research Centre

A THIEF CAN STEAL YOUR CAR IN AS LITTLE AS TWO MINUTES. A SMASH AND GRAB ROBBERY CAN HAPPEN IN SECONDS. IF YOUR CAR HAS A GPS DEVICE WITH YOUR HOME ADDRESS PROGRAMMED INTO IT, A THIEF CAN ROB YOUR HOME TOO!

One recent story involved a car break-in at a local sporting event. The thieves targeted cars in the fan parking lot knowing the owners would be watching the big game. A window was smashed and some money, a portable GPS unit and a remote garage door opener were stolen.

The thieves used the GPS system to guide them to the house. Then they used the remote control to open the garage door and gain entry to the house. Since the thieves knew what time the game was scheduled to finish, they had tome to clean out the house.

Thieves are only interested in what’s quick and easy. If you make it hard for them to break in, they’ll just move on to the next target.

TIPS FOR YOUR CAR

- If you have a portable GPS system or remote garage door opener, hide them well or take them with you when you leave the car.

- If your GPS has a key or password lock, use it. If it doesn’t, don’t put your home address in it. Instead program a nearby address (like a store or gas station) so you can still find your way home if you need to, but a thief can’t find out where you live.

TIPS FOR YOUR HOME

- Lock your doors. Even the best lock can’t protect you if you don’t use them.

- Be seen and safe. Trim hedges and bushes so your home is visible from the street.

- Know your neighbours. Neighbours who look out for each other are among the best, and least expensive, defence against crime.

- Keep it well lit. Make sure all outside entrances-front, back and side-have good lighting so burglars can’t easily hide.

Install a monitored alarm system. An alarm provides great protection against burglary and fire, but only if you use it.

by Eddie Rodriguez, CAIB | Jul 26, 2014 | Research Centre

DON’T LET A TORNADO BLOW YOUR ASSETS AWAY

ON AUGUST 21, 2011, THE FIRST F3 TORNADO IN OVER 15 YEARS HIT THE LAKESIDE TOWN OF GODERICH, ONTARIO, CAUSING OVER $75 MILLION DOLLARS IN DAMAGE. LIKEWISE, ON JUNE 6, 2010, AN F2 TORNADO WENT FROM HARROW THROUGH KINGSVILLE AND LEAMINGTON, ONTARIO, BEFORE DISSIPATING NEAR POINT PELEE NATIONAL PARK, CAUSING $120 MILLION DOLLARS IN DAMAGE.

These tornadoes are a vivid reminder of the threat windstorms pose to life and property, as well as emphasize the importance of having the right insurance coverage.

No matter where you live, you need to have the right amount and type of insurance in order to recover financially after a natural disaster.

Across Canada, Ontario, Alberta, Manitoba and Saskatchewan average the most tornadoes per season, at approximately 15, followed by Quebec with less than 10. New Brunswick and the interior of British Columbia are also recognized tornado zones. All other provinces and territories have significantly less threat from tornadoes. The peak season in Canada is in the summer months when clashing air masses move north, although tornadoes in Canada have occurred in spring, fall and in the rarest of cases, winter. This differs from the United States’ southern-central plains, when spring is the most prominent season for tornadoes.

For a variety of reasons, such as Canada’s lower population density and generally stronger housing construction, due to the colder climate, Canadian tornadoes have historically caused fewer fatalities than tornadoes in the United States.

The standard homeowners and business insurance policy covers wind damage including that caused by tornadoes to the structure of the building and contents including broken windows and removal of debris.

However, you should make sure your coverage limits reflect the cost of rebuilding the structure, removing the debris and fully replacing personal belongings.

It’s important to make sure you have purchased ‘replacement cost coverage’ on your business policy and your homeowners’ insurance policy. If you have a business policy, it is also important that you carry ‘blanket bylaws coverage’ on your policy.

A homeowners’ policy also provides ‘Additional Living Expense (ALE) coverage’ to pay the costs of living away from home if you cannot inhabit your house due to damage from an insured disaster.

The policy ALE provision covers hotel bills, restaurant bills, and other living expenses incurred while away from your home, while it is being repaired or rebuilt.

‘Guaranteed Replacement Cost (GRC)’ or ‘Additional Rebuilding Cost (ARC)’ is another homeowner’s insurance coverage that can provide extra coverage, over and above the limit you have on your home insurance policy.

For example, let’s say you have your home insured for $400,000 – a tornado destroys 200 homes in your area, and building costs and inflation cause the replacement of your home to be $450,000. The GRC and ARC coverage’s would pay this additional amount subject to the terms and conditions of your policy. Make sure you review these coverages with your broker.

If you own a business that has been damaged, ‘business interruption coverage insurance’ is important to make sure you have revenue to continue to make your payments when a tornado has impaired your business. There are many different forms of business interruption, and as a business owner, you should review this on a regular basis with your insurance broker.

Damage to cars, trailers, motor homes and ATV’s are covered under the ‘comprehensive optional coverage’ portion of the policy. Marine insurance policies will usually cover damage to boats from wind.

Please make sure you review your insurance policies with your insurance broker on a regular basis to make sure your assets don’t get blown away, should a Tornado destroy or damage your home and business. With changing weather patterns, your home could be the next target.

For more information on your coverage options, call your insurance broker.

by Eddie Rodriguez, CAIB | Jul 26, 2014 | Research Centre

WATER DAMAGE CLAIMS HAVE BECOME A BIG PROBLEM FOR CANADIAN HOMEOWNERS. REASONS FOR THE INCREASE CAN BE TRACED TO CLIMATE CHANGE, LIFESTYLE CHANGE AND AGEING INFRASTRUCTURE. MOST HOMEOWNER POLICIES COVER WATER DAMAGE THAT HAPPENS SUDDENLY AND ACCIDENTALLY, BUT MAY NOT COVER SEWER BACKUPS (WHERE SEPARATE COVERAGE IS NEEDED).

Slow leaks and water seepage that occur over time may also not be covered; quite often they’re considered home maintenance.

And if a flood happens from a local river swelling, you’re likely not covered for that either. So. What to do? Prevention! The first place to start is your sump pump. How old is it? When was the last time you checked it? To ensure it’s working properly, lift the cover and slowly pour water into the sump tank; watch for the float to rise and trigger the pump to activate. Once the water level is lowered, the pump should turn off. Additional tips:

- The pipe that carries the water out of your house should be at least 2 meters from the building, and the water should flow away from your house

- A battery backup is great to have in case of a power failure – make sure the battery is always fully charged

- Remember to check your roof – is it reaching its best before time? If in doubt, have a professional roofer take a look

- Make sure any belongings that are stored in your basement are placed in plastic bins located off the floor

- If you’re converting your basement to a living area, use water resistant materials

What about lifestyle?

Things like dishwashers, hot tubs, hot water heaters, washing machines and water-dispensing fridges are all appliances that have the potential to leak.

Keep an eye on your water bill. If it seems it’s increasing without reason, check the hoses and connections to your appliances. If they’re plastic, consider changing them to CSA approved stainless steel braided hoses. And consider having someone take a look at your hot water heater – their life span is usually only ten years.

Need advice? Call in a professional for recommendations and ask your insurance broker to confirm what’s covered in your policy.