by Eddie Rodriguez, CAIB | Nov 14, 2014 | Featured, Research Centre

http://youtu.be/G_MzHwufAfk

We’re pleased to announce the launch of the my Driving Discount™ program: the smart road to savings!

Some people have better driving habits than others. The program rewards good driving behaviour.

The my Driving Discount™ program is available exclusively to clients insured through Intact Insurance.

With my Driving Discount™ , you could save up to 25%* off your car insurance premium. Enrolling is quick and easy and you’ll automatically get a 5% … 10% discount when you sign up.

How Does it Work?

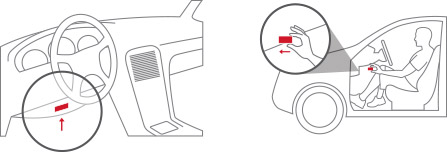

Contact us online or call our office at 416-255-3728 to sign up. Once enrolled, you will receive your device in the mail.

Simply plug this into your car and it will record your driving behaviour including:

- braking,

- acceleration

- and time of day you drive.

The reported data is used to calculate a personalized discount of up to 25% off your car insurance premium. Once you complete your initial assessment period (minimum of 180 days) your earned discount will be applied to your policy at your next renewal. But that’s not all ….

You’ll also be able to view your driving data and your potential discount on your own personalized website.

Key Benefits:

- Save immediately! Get a 5% … 10% enrollment discount just for signing up

- Earn up to 25% discount at renewal (minimum of 180 days monitoring required)

- Customized car insurance premium that reflects the way you drive

- Nothing to lose, your premium won’t increase based on the data collected

- Personalized website that shows your driving behaviour and discounts

- Small, easy to install device

The my Driving Discount™ program is available exclusively to clients insured through Intact Insurance.

Frequently Asked Questions

1. What factors are taken into consideration when calculating my potential discount?

my Driving Discount™ could reward you with a personalized discount by assessing the time of day that you drive, along with your acceleration and braking, based on the kilometres driven.

Hard Braking: Hard braking increases the risk of being involved in an accident. The program therefore calculates the ratio of hard braking events on total km driven to determine your personalized hard braking factor. A hard braking event is defined as any decrease of speed of 12 km/h or more in less than 1 second.

Hard Braking: Hard braking increases the risk of being involved in an accident. The program therefore calculates the ratio of hard braking events on total km driven to determine your personalized hard braking factor. A hard braking event is defined as any decrease of speed of 12 km/h or more in less than 1 second.

Rapid Accelerating: Rapid accelerations increase the risk of being involved in an accident. The program therefore calculates the ratio of rapid acceleration events on total km driven to determine your personalized rapid acceleration factor. A rapid acceleration is defined as any increase of speed of 12 km/h or more in less than 1 second.

Rapid Accelerating: Rapid accelerations increase the risk of being involved in an accident. The program therefore calculates the ratio of rapid acceleration events on total km driven to determine your personalized rapid acceleration factor. A rapid acceleration is defined as any increase of speed of 12 km/h or more in less than 1 second.

Time of day: Driving at night (between 12 a.m. and 4 a.m.) increases the risk of being involved in an accident. Many elements, such as reduced visibility and fatigue, make this time of day the riskiest. The program therefore evaluates the time of day that you’re driving to determine your personalized high-risk period factor. The less you drive at night the more you could save.

Time of day: Driving at night (between 12 a.m. and 4 a.m.) increases the risk of being involved in an accident. Many elements, such as reduced visibility and fatigue, make this time of day the riskiest. The program therefore evaluates the time of day that you’re driving to determine your personalized high-risk period factor. The less you drive at night the more you could save.

2. When will I receive my personalized discount?

If you are eligible for a personalized discount, your premium will be adjusted at renewal upon the completion of your assessment period.

3. How long is my assessment period?

Your initial assessment period is for a minimum of 180 days from when you install your device and start driving.

If the assessment period cannot be completed prior to when your renewal is issued (not the effective date of the renewal) , then the renewal will be issued with your 5% enrollment discount. The personalized discount will be applied upon the subsequent renewal.

4. How long will my personalized discount apply?

Your personalized discount is not static and is subject to change upon each successive renewal of your policy. All successive discounts will be calculated based on the previous 12 months of data collected to assess your driving habits.

5. If I have to brake hard to avoid an accident, will that reduce my discount?

We look for the frequency of events and regular driving behaviours. We know that even the best drivers have to brake hard occasionally. So it doesn’t necessarily mean that if you brake hard once, your discount will be reduced.

The most important thing is your safety. If you need to hard brake to avoid an accident, make sure you do!

6. Can my premium go up because of my driving habits?

No, your premium will not increase as a result of the data used to calculate your discount (time of day you drive, braking, and acceleration). For complete details on how your data is used, please refer to the Terms of Use.

7. What happens if I have an accident while using the my Driving Discount device?

Accidents are not taken into consideration when calculating your potential personalized discount.

However, this may nevertheless have an impact on your insurance premium as per our standard practices If you have questions about your policy or premium, please contact us.

8. How is my driving data used?

The collected driving data will be used to determine your eligibility and potential discount following your assessment period.

We may also analyze the collected driving data to ensure consistency with your policy, and you may be contacted by your broker to see if you wish to discuss your policy further.

9. Can I change my mind and opt out of the program? If so, will my insurance policy be cancelled?

Yes. You may opt out at any time.

Your insurance policy will NOT be cancelled even if you opt out of my Driving Discount program. The program is optional. Please contact us if you have any questions.

10. Can multiple principal drivers on the same policy enrol in the my Driving Discount program?

Yes. Every principal driver on the policy can enrol if they meet the eligibility criteria.

[hr]*Certain conditions, limitations and exclusions apply.

® Intact Insurance small straight lines design is a registered trademark of Intact Financial Corporation.

TM my Driving Discount is a trademark of Intact Insurance Company. © 2014, Intact Insurance Company. All rights reserved.

by Eddie Rodriguez, CAIB | Jan 28, 2013 | Featured, Research Centre

It’s a fact: as you attempt to achieve your company’s goals, you will naturally take a number of risks that may bring about accidental losses to your property, to your income, through liability to others, etc.

Perish the thought!

The harsh reality is that, unless you are properly prepared to prevent these losses – and to “transfer” them to an insurance company when they do happen – the consequences could completely destroy or cripple your business. That’s why we prefer to call “risk exposures” and their potential consequences:

“The Monsters“

Calling them “The Monsters” helps us remember that these are not simply words you find on some “risk assessment report” that lies forgotten on your company’s intranet.

So, with the goal of helping you become aware of some of the monsters you need be on the look out for, let’s take a look at 8 loss scenarios specific to technology companies.

By the way, if you’re thinking “I’m fine. I have business insurance”, just remember that a General Liability insurance policy (which is the most common type of insurance a business would carry), would NOT protect you in the scenarios listed below. That’s because General Liability is there to protect you only against claims of property damage and bodily injury .

Tip: As you read each example below, ask yourself: Could this particular Monster attack my business? What are we doing (other than insurance) to mitigate the consequences of this Monster’s attack? Do we have the proper insurance protection for this scenario?

OK, here we go:

Errors and Omissions in general:

The first monster that IT companies and IT professionals must be aware of is the infamous “E & O” monster.

‘E & O” stands for Errors and Omissions, aka Professional Liability …. or, as it is known in other fields, “Malpractice liability”.

It’s usually your clients who will wake up the “E & O” Monster and send it out to get you, when they feel that the financial loss they’ve just suffered was caused by:

– your company’s ERROR (something you did wrong) or….

– an OMISSION (something you, a as professional, should have done, but didn’t).

The “E & O” Monster also visits you when, for example, your client claims that your product failed to perform as expected.

What really sucks is that you can be sued, even if you didn’t make a mistake!

For example, let’s say you design a new invoicing system for a client and the client alleges the final system lacks the functionality they wanted. This happens, even though you delivered what you thought was required. If your client sues you (and you have the right insurance coverage) your insurance company will defend you, which protects you from having to pay the potentially huge ‘defense costs’.

Monster # 2: Where’s My Data? *

How did “corrupted data” create a $900,000.00 loss for a software vendor?

A communications company sues for lost revenue and expenses to recover billing files for wireless customers.

The billing files were deleted by their software vendor while updating the system.

Indemnity Paid: $750,000 / Defense Costs Paid: $150,000

Monster # 3: Software Fails to Maintain Employee Hours *

A company provides timekeeping hardware and software to its customer.

The software doesn’t function correctly; it fails to maintain employee hours worked and correctly apply the hourly and overtime rate of pay.

The failure results in over/underpaying employees and the need to replace the timekeeping clocks. The customer sues the provider of the hardware and software.

Indemnity Paid: $440,000

Monster # 4: Missed deadlines cause a breach of contract *

It’s was time for a company-wide upgrade, and a firm decided to outsource to an information technology and management services company all the replacement of hardware, software and infrastructure as well as telecommunications and related services in order to upgrade its ability to serve customers and address any problems.

The information technology and management services firm fails to meet deadlines due to a high turnover of staff and a breakdown of project management.

Indemnity Reserve: $2,000,000 / Expense Paid: $500,000

Monster # 5: Breach of Security *

A telecommunications firm is sued by customers claiming they were sold a defective system with inadequate security protections.

The customers claim the faulty system allowed individuals to access their phone system and, as a result, they incurred fraudulent overseas charges.

Indemnity Paid: $345,000

Before we move on, here a couple of interesting facts about data breach losses:

Based on a sample of 900 breaches reported to insurance companies 86% of the data breaches were discovered by third-parties (not by the companies whose systems had been breached), and 96% were avoidable with simple precautions.

Monster # 6: Defending software that performed as promised *

How about getting sued when you have not done anything wrong and your product performs as expected?

A software company was sued by a customer after he used the company’s cost estimating software.

The software itself was found to have functioned perfectly. The error was on the part of the user who later underbid a work project. The customer eventually dropped the case, but only after considerable legal expenses were incurred by the software company.

Indemnity Paid: $0 / Defense Costs Paid: $175,000

Monster # 7: Inability to deliver on marketing “promises” *

A personal computer assembler is sued by a group of consumers in a class action suit.

The suit alleges that the company’s equipment did not live up to advertised specifications. Citing issues such as lack of speed and poor upgrade capability, the consumers demand full refunds.

Indemnity Paid: $1,600,000

Monster # 8: Web design and integration services * *

Our policyholder was hired to create an e-commerce website for

trading and selling valuable collectibles. The client later alleged that our policyholder failed to deliver a working website and negligently recommended that the client purchase Web-enabling software from another company that then abandoned the project and the software.

Indemnity Paid: $180,000

Defense Costs Paid: $558,928

* Loss Scenarios (examples) marked with * provided by Chubb Insurance Company of Canada.

* * Loss Scenarios (examples) marked with ** provided by Travelers Canada.

I’ve limited this article to the brief explanation about Errors and Omissions and the other 7 loss scenarios because I know that most people won’t be naturally inclined to reading about insurance.

But when you think about it, being able to learn about real-life examples of what could happen to your business (without actually experiencing it) is a very simple way to identify potential risks ….. and that, my friend, is precisely step #1 to implementing a good risk management plan.

Insurance can help you when/if bad stuff happens. But there’s tons of stuff you can do, aside from purchasing insurance, to protect your business.